》Check SMM aluminum product quotes, data, and market analysis

》Subscribe to view historical prices of SMM metal spot cargo

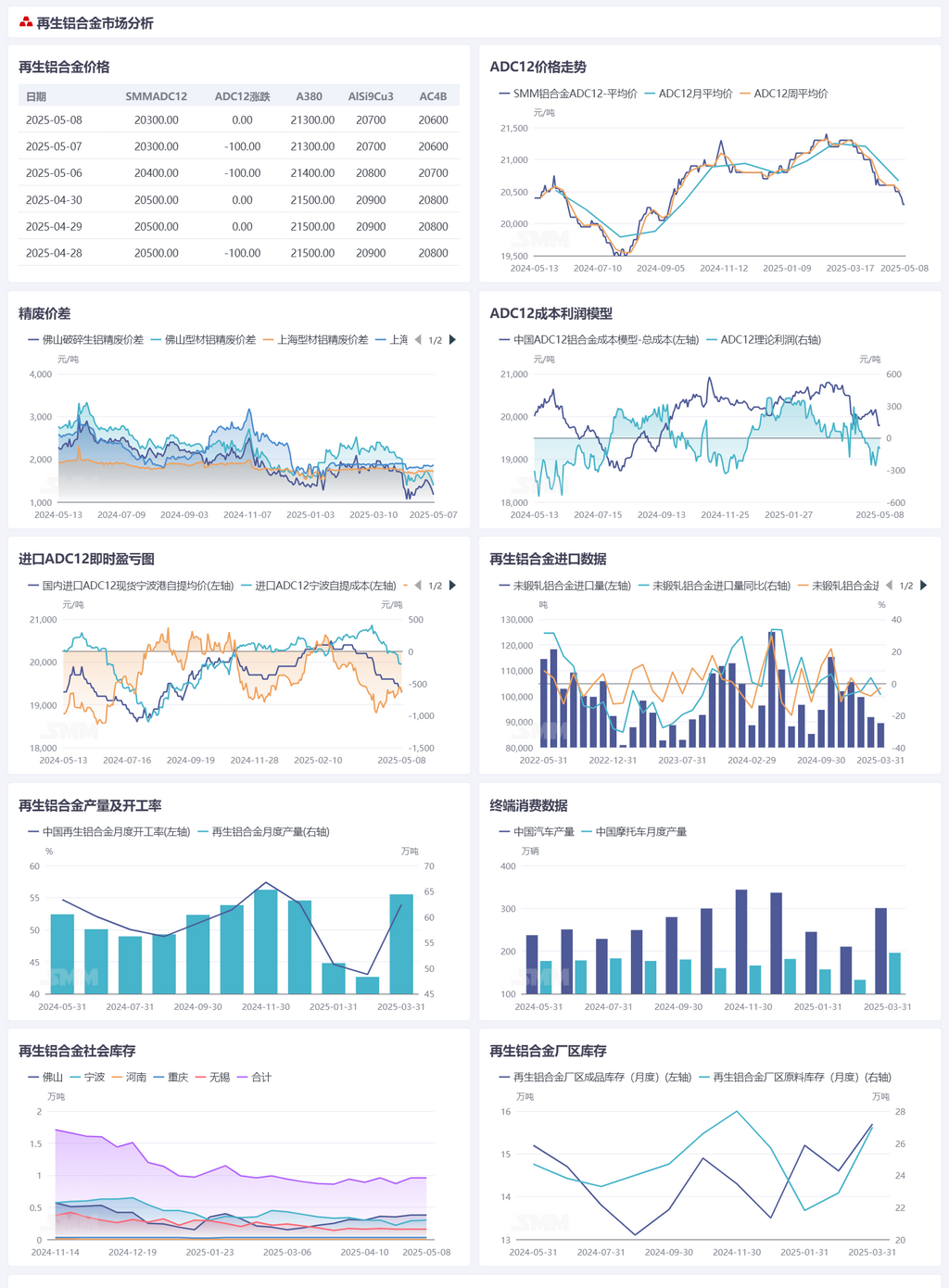

Secondary aluminum raw materials:

The aluminum scrap market showed a differentiated adjustment trend after the Labour Day holiday. As of May 8, SMM A00 primary aluminum spot closed at 19,620 yuan/mt, down a cumulative 440 yuan/mt from before the holiday (April 30). Aluminum scrap prices generally followed the decline in primary aluminum, but there were significant differences by grade and region. By product, the price of baled UBC fell from 15,050-15,650 yuan/mt (tax excluded) before the holiday to 14,800-15,400 yuan/mt, with a cumulative decrease of 200 yuan/mt during the week. However, in Jiangxi and other places, the decline was narrowed due to higher recycling prices, and some wrought aluminum alloy scrap prices were resilient due to tight supply. The supply of aluminum tense scrap products was tight, and the price range of shredded aluminum tense scrap slightly shifted downward from 15,850-17,350 yuan/mt before the holiday to 15,650-17,150 yuan/mt. Regionally, quotes in Hunan, Jiangxi, and South China remained firm, with price adjustments lagging behind primary aluminum. East China and central China closely tracked aluminum prices, with a decrease of 100-150 yuan/mt during the week. On the demand side, constrained by weak orders from downstream processing enterprises, the operating rate of secondary aluminum enterprises declined, and procurement was mainly for just-in-time needs. The price difference between A00 aluminum and aluminum scrap fluctuated more sharply. The price spread of mechanical casting aluminum scrap in Shanghai narrowed to 1,871 yuan/mt, and the price spread of mixed aluminum extrusion scrap free of paint in Foshan decreased to 1,386 yuan/mt, reflecting stronger cost support for aluminum scrap. Looking ahead, the aluminum scrap market may continue to fluctuate at highs. The tight supply situation for aluminum tense scrap products is unlikely to change, providing strong price support. Wrought aluminum alloy scrap prices will still be dominated by fluctuations in primary aluminum and are expected to adjust within a narrow range. Going forward, attention should be paid to macro risks such as a policy shift by the US Fed and geopolitical conflicts, which may trigger sharp fluctuations in primary aluminum, or to concentrated production cuts by domestic secondary aluminum enterprises, which may put pressure on aluminum scrap prices.

Secondary aluminum alloy:

This week, the center of aluminum prices moved downward, and secondary aluminum alloy prices maintained a downward trend. As of May 8, the SMM ADC12 price fell by 200 yuan/mt from before the holiday to the range of 20,200-20,400 yuan/mt. On the cost side, despite the decline in aluminum scrap and silicon metal prices pulling down the production cost of ADC12, the cost support was strengthened by traders standing firm on quotes due to the contraction in aluminum scrap circulation. Sustained pressure on the demand side became the main factor constraining prices. Post-holiday market transactions were relatively sluggish, with downstream enterprises mainly making just-in-time procurement and a small amount of restocking for just-in-time needs. Moreover, the continuous decline in aluminum prices exacerbated market wait-and-see sentiment. In addition, after entering May, the characteristics of the traditional off-season gradually emerged, coupled with the impact of tariffs, leading to a reduction in both domestic and overseas orders. In terms of supply, the operating rate of secondary aluminum plants showed a slight recovery after the holiday. However, under the dual pressure of high costs and insufficient orders, some enterprises chose to cut or even halt production to stop losses. It is expected that the industry's operating rate will continue to decline in May.On the import front, overseas ADC12 prices were adjusted downward this week to the range of US$2,410-2,440/mt. The immediate loss for imported ADC12 was around 600 yuan/mt, and the import window remained closed. Overall, the current secondary aluminum market is in a phase of contention between cost support and weak demand. In the short term, ADC12 prices may continue to fluctuate rangebound. In the later period, close attention should be paid to the supply situation of aluminum scrap and the pace of improvement in end-use consumption. If the raw material side maintains a tight supply situation and aluminum prices stabilize, ADC12 may reach a phased bottom. However, before a substantive recovery in demand, price increases will still be suppressed.